The first forced buyers arrive today, and the stock has already run to meet them

Marking the pre-IPO call to market: an updated forced-bid number, a new options market pricing the inclusion more honestly than the cash tape, and why the real cliff is still in August.

Update, 2026-06-18. A second note after the piece written before the IPO.

Last week I argued three things about the SpaceX inclusion: that the realized forced bid would be a lot smaller than the headline figures, that most of the price move would arrive before the funds actually bought, and that the real turn would come in August when the lockup starts to unwind. That piece got a lot more attention than I expected, in good part because Toby Nangle kindly included it in FT Alphaville's Further Reading list on Monday. Many thanks to him. The first mechanical wave finally hit today, Thursday June 18, when funds tracking the CRSP US Total Market and the FTSE Russell indices added SpaceX at the close. It is a good moment to mark the call to market, update the numbers with live data, and say what I think happens next.

Live scoreboard · June 18, 2026

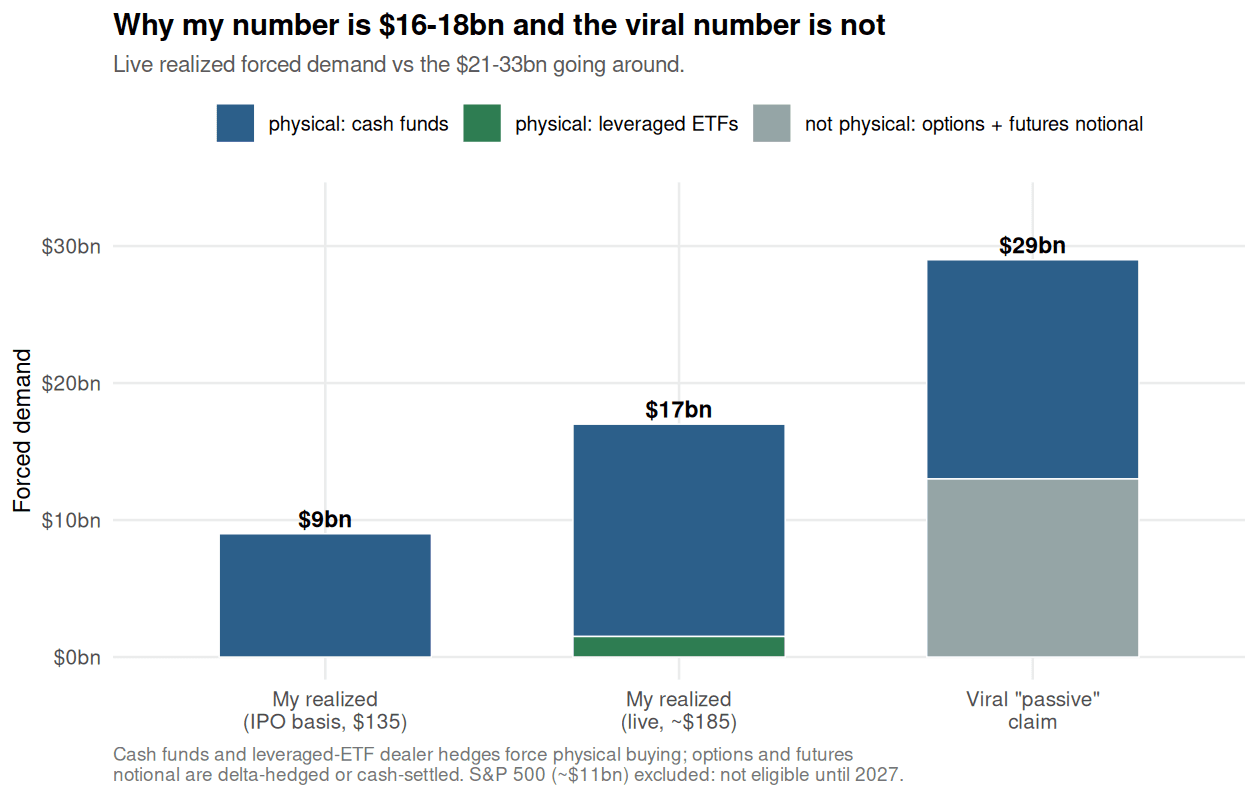

For context, the same realized bid was about $9bn at the $135 IPO, about 12% of float, against the mid-teens today.

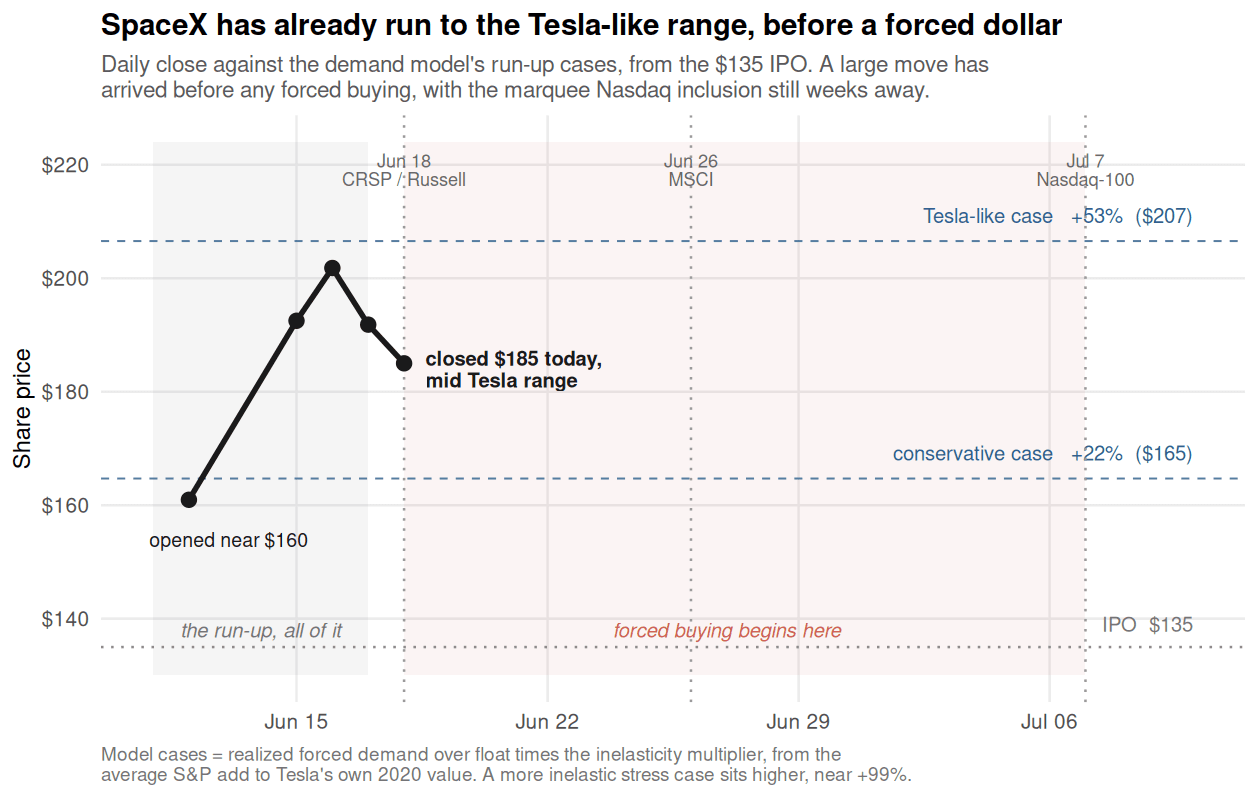

Here is the short version. SpaceX priced at $135 and closed today near $185, about 37 percent above the IPO, after a violent round trip: it opened near $188, washed out to the low $170s intraday, then rallied hard in the final half hour to tag $190 before settling back to $185, down about 4 percent on the day. It had printed above $210 only yesterday. The entire run to here came before a single index fund was forced to buy a share, and the first forced buying landed only at today's close. The whole move so far is pure anticipation, exactly the pattern I argued for. The interesting part is what has grown up around the name in a single week. It now has an options market that is pricing the situation far more honestly than the stock tape: around 90 percent implied volatility and a skew that flipped in a day from fearing the lockup to chasing the inclusion. The headlines are still arguing about the wrong number, a forced bid that is real but nowhere near the $30 billion going around. And the history of these events says it is not over: across hundreds of past inclusions the run keeps building right up to the day the funds actually buy, and the biggest date on SpaceX's calendar, the Nasdaq-100 on July 7, has not arrived. The real cliff comes later still, in August, when the lockup cracks. Here is how the rest of it goes.

The number, updated: about $16 to $18 billion, and still not $30 billion

My estimate before the IPO was a realized forced bid of about $9 billion, roughly 12 percent of float, on a $135 stock and the fund assets I could measure as of late 2024. Both inputs are now stale in the same direction. SpaceX closed near $185, and the index funds that must hold it are far larger than they were eighteen months ago. Repricing SpaceX's float weight at the current price and live fund assets, the realized forced bid is about $16 to $18 billion, in a $15 to $20 billion range.

The important thing is what did and did not change. The dollar figure jumped for two boring reasons: the stock is about 37 percent higher than the IPO, and the funds that must hold it are far larger than they were in 2024. The forced position as a fraction of float, which is the metric that actually measures pressure, rose only modestly, from my pre-IPO 12 percent to the mid-teens; in shares it is on the order of 85 to 95 million, against the roughly 67 million I first estimated. Most of the jump from a $9 billion figure to a mid-teens-of-billions one is repricing and fund growth, not a dramatically larger claim on the company, and a mid-teens percent of float, bought over weeks against a float that turns over in a day, is still not the pressure the raw dollar number implies.

That distinction is the whole disagreement with the figures still circulating, some of which now run to $21 to $33 billion of “passive forced buying.” Those come from taking the roughly $1.4 trillion that Nasdaq says is benchmarked to the Nasdaq-100 and multiplying it by SpaceX's weight. But that $1.4 trillion is about half cash funds and half derivatives, and most of the derivative half does not buy a single share at inclusion.

And the single largest line in the press version, the S&P 500, is not coming at all: SpaceX fails the profitability test and is not eligible before 2027, which quietly removes roughly $11 billion of assumed demand.

The schedule, with today at the front

These are the mechanical figures by provider. For the broad-market waves the realized bid is roughly half of each, after the active manager haircut; the Nasdaq event is the exception, where it is realized almost in full because the trackers are pure index funds.

- Today, Thursday June 18 (its fifth trading day): the fast entry additions to the CRSP US Total Market (~$4.6bn) and the FTSE Russell US and global indices (~$6.1bn), plus the S&P total market suite (~$1.1bn). About $11.8 billion mechanical, the largest gross wave. Outside analysts put this dual event at $10 to $16 billion; my realized read is closer to $6 to $9 billion of it, because so much of this money is active and only partly tracks.

- June 26: FTSE Russell's annual reconstitution reweights the name, and MSCI's global and US standard indices add it around the end of the month. On the order of $2.5 billion.

- July 7: the Nasdaq-100, the headline inclusion, which triple weights SpaceX under its thin float cap rule and now carries a verified weight near 0.7 percent at the IPO price, about 1.0 to 1.1 percent at today's price. The two dominant trackers, QQQ and QQQM, are about $590 billion between them and must take SpaceX at that capped weight, roughly $6 to $7 billion of cash demand, plus another ~$1.5 billion of leveraged-ETF hedging, about $8 to $9 billion mechanical. Crucially, QQQ and QQQM are pure index funds, so almost none of it is haircut away: in realized terms it rivals the entire June 18 wave, but concentrated in one fund family on a single day.

One number worth holding next to all of these: SpaceX traded more than 320 million shares on Tuesday alone, against a float of roughly 556 million, and even the calmer sessions since have turned over well over a hundred million shares a day. The float changes hands in a day or so. The entire forced index purchase, ever, is less than a single morning of current volume. Whatever the inclusion does to the price, it will not be because the funds cannot find the stock.

What the options say, which is more than the stock does

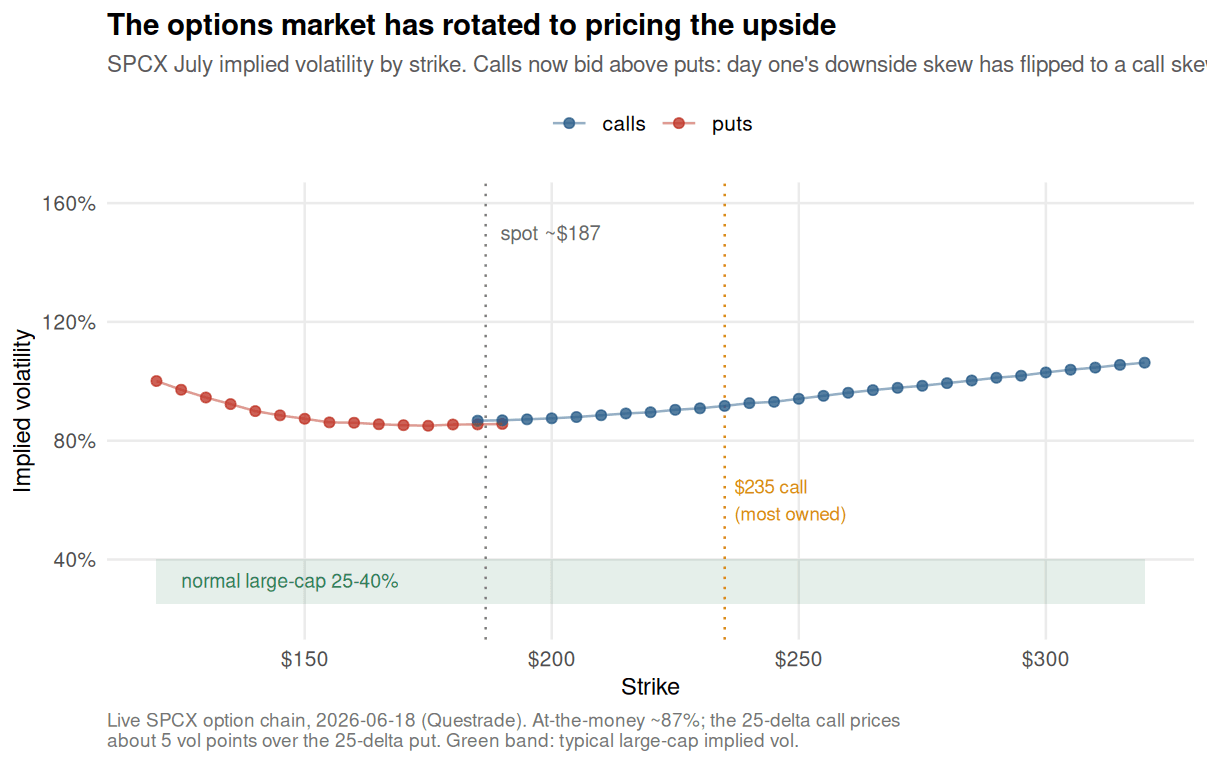

The most informative development since the first piece is that SpaceX got an options market on Tuesday, and it is pricing the situation far more honestly than the cash tape.

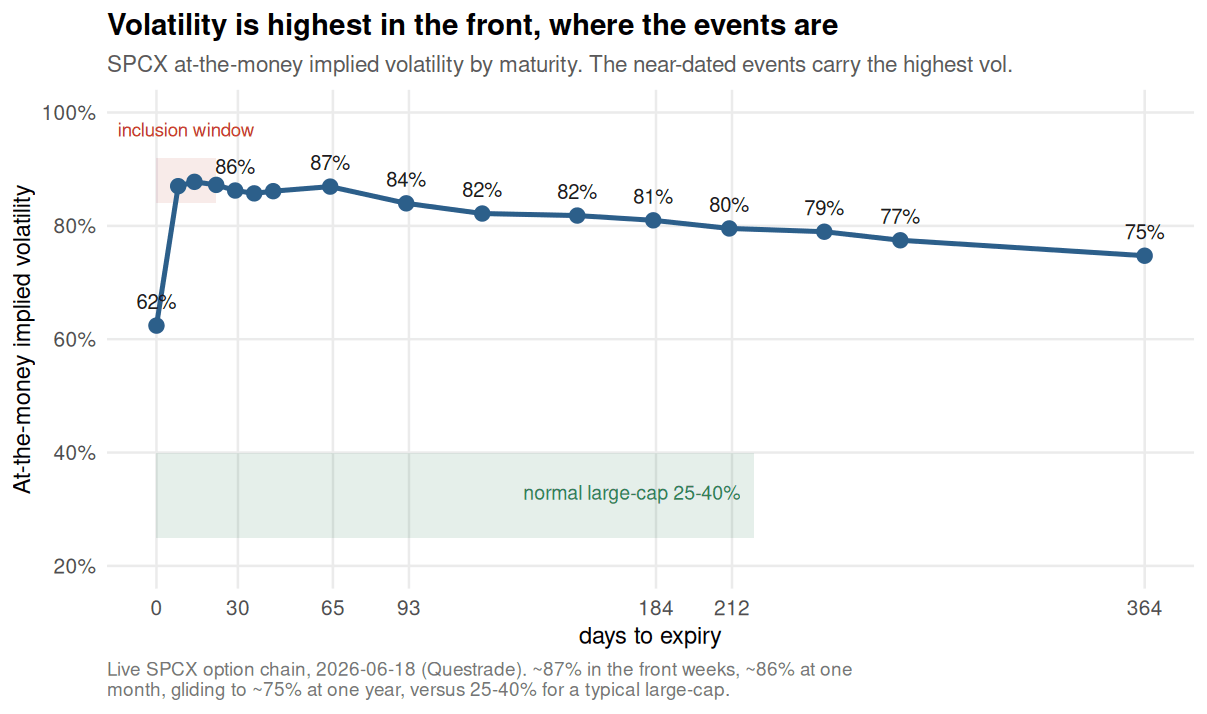

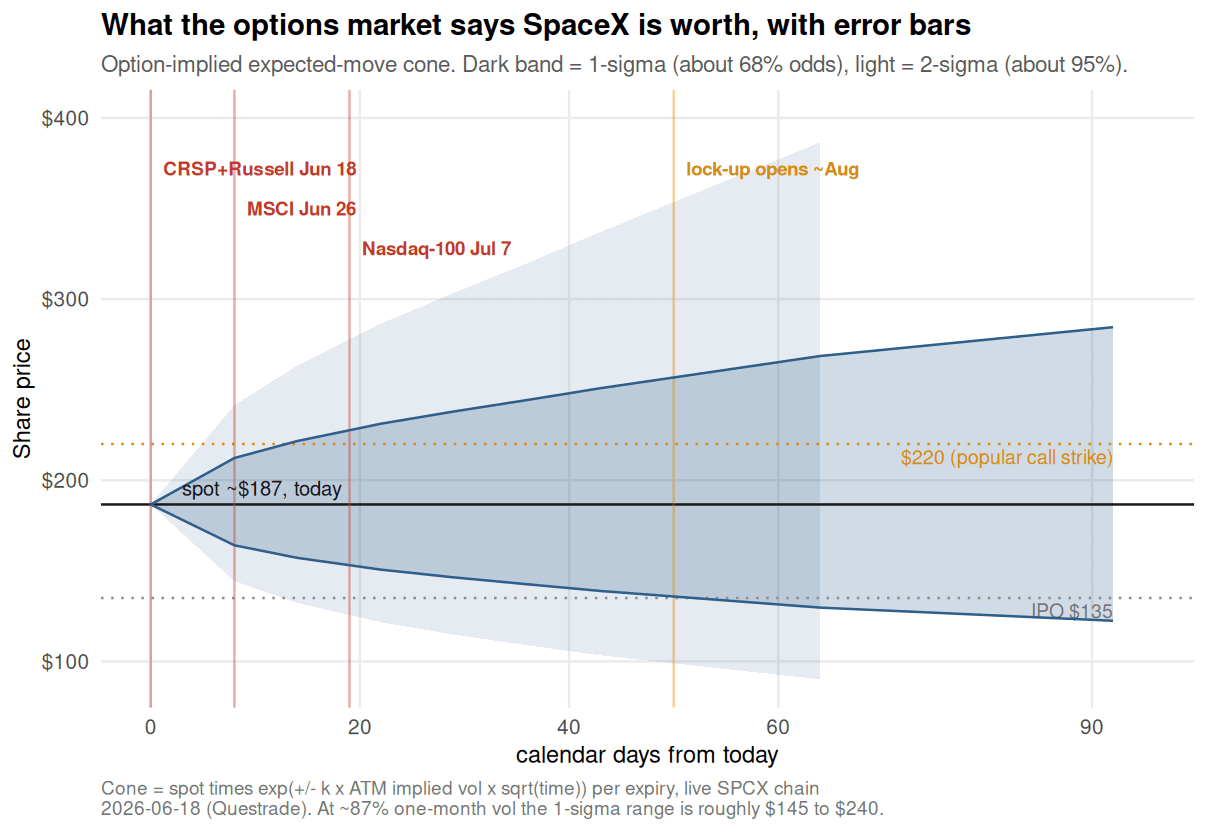

Implied volatility opened around 110 to 115 percent on Tuesday and sits near 87 percent at the money in the front month today, against 25 to 40 percent for a typical large-cap. The whole surface slopes down with maturity: about 87 percent in the front weeks, 86 percent at one month, and a steady glide to about 75 percent a year out. The one-day contract expiring into today's close has already deflated toward 60 percent, the inclusion-day uncertainty resolving as the forced flow turns into known quantity. That downward term structure is the market saying the same thing the calendar does, that the next few weeks, the inclusion window and the run into the first earnings, are the uncertain part, and that the uncertainty slowly bleeds off as the lockup resolves the float.

What has changed in just a day is the skew, and it is the most interesting tell on the surface. On day one the puts were bid far above the calls, a classic downside fear skew, the market paying up for protection against the lockup cliff. By today that has flipped. The wings now tilt the other way: 25 delta calls price about 5 volatility points above the equivalent puts in the front month, and calls sit above puts at nearly every tenor out past six months, the call premium widest in the one-to-two-month contracts and fading as you go further out. In plain terms, the option market has rotated from paying for downside to paying for upside, and it is paying most for the upside that lands right on the inclusion dates. That is the signature of a crowd positioning for an inclusion day gamma squeeze, and it sits directly on top of a cash tape that round-tripped violently today, washing out to the low $170s and then surging late to tag $190 before closing at $185, down on the day yet bid hard into the bell. The euphoria and the fear are now stacked in the same chain at different horizons: an upside squeeze priced into the front, the lockup supply still lurking in the back where the skew flattens out.

The euphoria is loud in the flow. The most heavily owned contracts are upside calls, the $235 and $225 strikes, with tens of thousands of $210 calls that expire today changing hands, and there is open talk of a dealer gamma squeeze toward $400 if the buying continues. So the option market is doing two things at once: it is crowding the inclusion day upside while the deeper surface still carries the memory of the supply cliff to come. Both can be true. They usually are right before a scheduled supply event.

There are now leveraged products on the name itself, not just on the index. Single stock 2x long and 2x short SpaceX ETFs began trading this week. They are small today, but they matter for the mechanics, because they add their own daily forced rebalancing, amplified by leverage, on top of the index flows, in the same direction as the move. And almost none of the float trades freely until the August lockup lifts, so there is no real stock-loan market yet, which is exactly the condition under which a forced bid translates into price rather than being absorbed. The arbitrage that normally flattens an index inclusion bump cannot run here at any size: you cannot short the rich leg cheaply, and the options that would substitute for it cost roughly 85 to 90 percent vol.

One note on the active managers, the other half of the mechanism. Across hundreds of past additions only about one active fund in twenty even holds a newly added name, and it adds far less than the full index weight. So today's bid is a passive one. Active managers are not the buyers, and not the sellers either; the shares come from the firm and the lockup, not from them.

The refined call: a lot is priced, but it is too early to call it over

Put the model next to the tape. My framework prices the premium as forced demand over float times an inelasticity multiplier, which gave a run of plus 22 percent on a conservative multiplier and plus 53 percent on one like Tesla's. The stock closed at $185, and it printed into and through that Tesla band as recently as yesterday, before a single forced dollar. So a good part of the move the model can predict looks priced already. I want to be disciplined about that conclusion, though, because two things cut against my own first instinct to say the move is done.

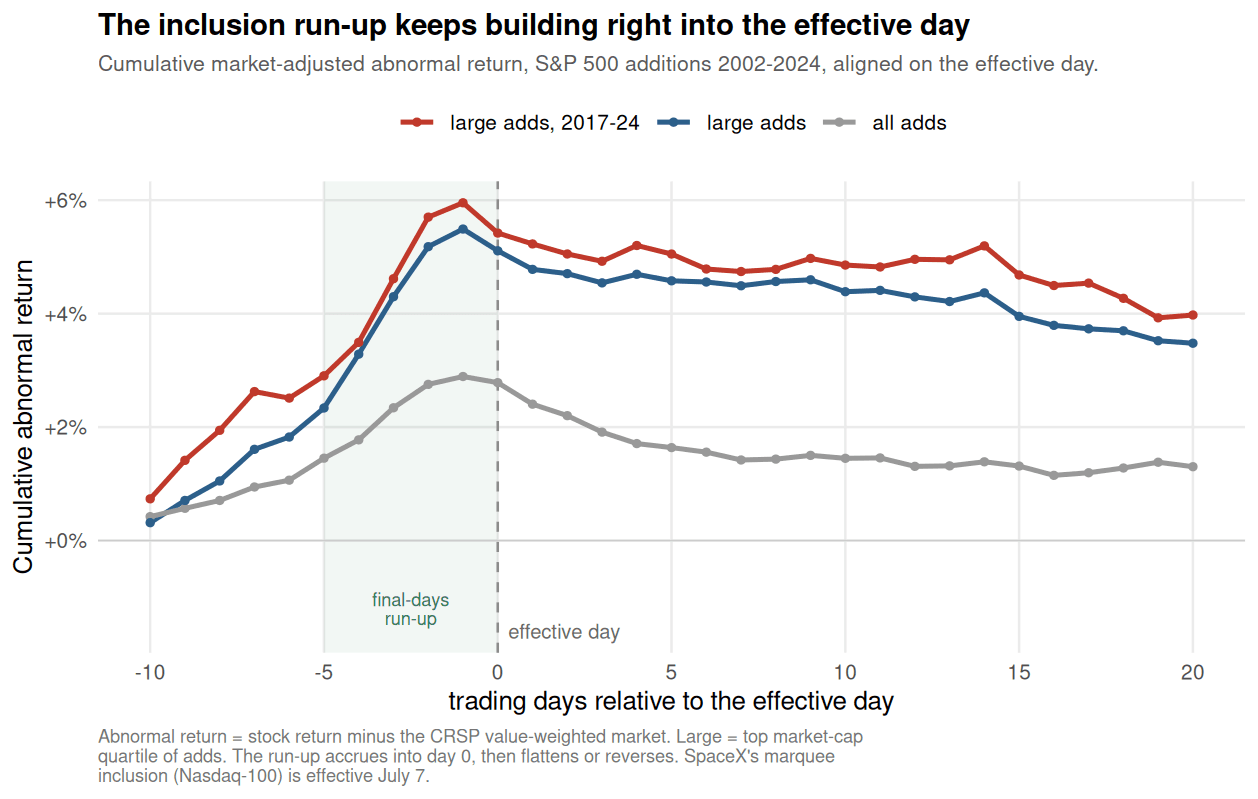

The first is the calendar. The biggest single forced demand event has not happened. The headline inclusion is the Nasdaq-100 on July 7, where the modified float rule triple weights SpaceX, and that is still three weeks out. And the historical pattern says the run keeps building right up to the effective day rather than finishing early.

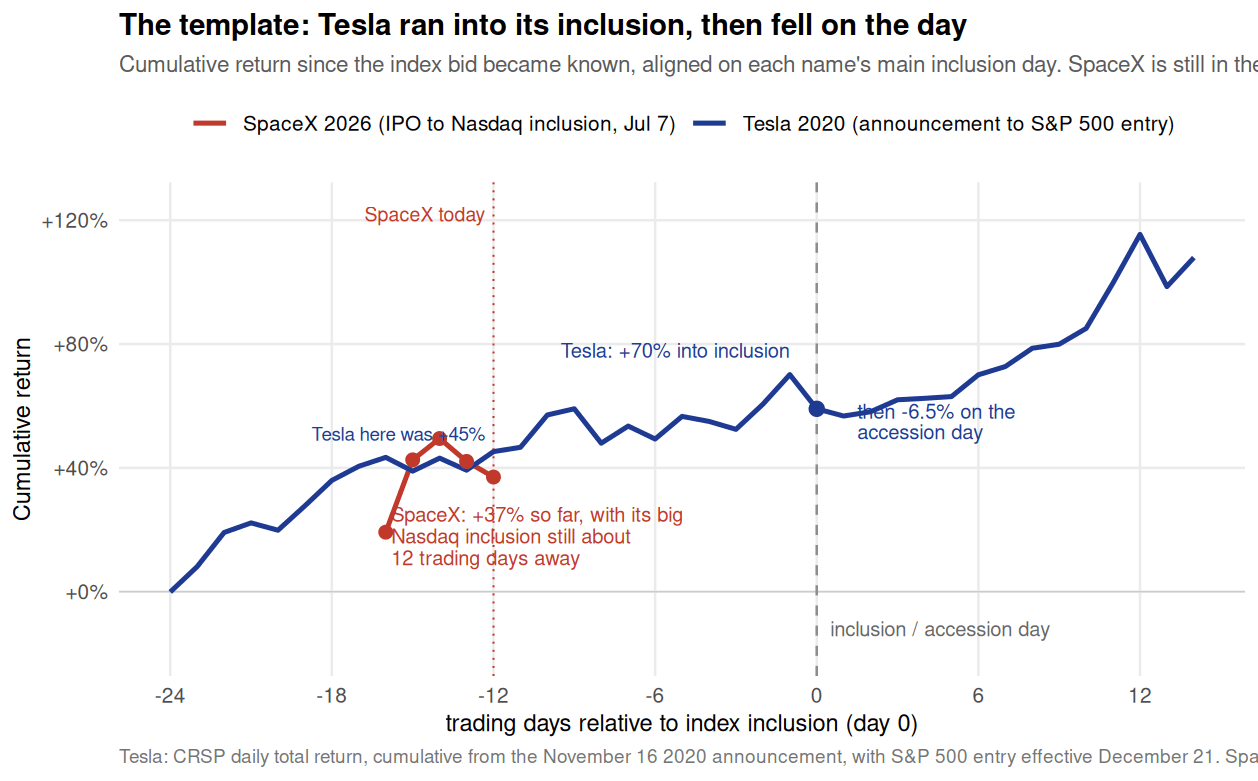

This is not just the Tesla story. Across 462 S&P 500 additions since 2002, lined up on the day they enter, the run keeps building right into the effective day. In the final week the average add earns about plus 1.9 percent over the market, and the biggest adds, the closest analog to SpaceX, plus 3.7 percent, a third of it in the last two days. The reversal comes on the day and after, not before: the effective day is slightly negative and the next month gives back about a point and a half. The premium arrives late. So the exit is into the strength of the effective date, not three weeks early, and the front running for the Nasdaq weight may still be ahead of us. For SpaceX that date is July 7.

The second is attribution. I cannot cleanly separate how much of the run is the forced buying running ahead, and how much is the ordinary churn of a listing only days old that happens to be one of the most famous private companies in the world. A brand new options market, single stock leveraged ETFs, and a wall of retail are all pushing at once, and momentum like that can carry a stock well past what any demand model would justify, in either direction. If forced demand is only part of what has moved the price, then the piece that specifically runs ahead of the Nasdaq weight is not necessarily spent. A clean decomposition of the flow, separating the mechanical bid from the hype, is the obvious next thing to do, and I would want it in hand before declaring the catalyst exhausted.

The Tesla analogy is worth seeing directly, because it is the closest precedent I have. In 2020 Tesla climbed about 70 percent from the day its S&P 500 entry was announced to the day before it took effect, then fell six and a half percent on the accession day itself, when the index funds finally bought and the fast money sold. SpaceX has done the same thing faster: a run of more than 40 percent compressed into a handful of trading days, then a soft first inclusion day, closing down about 4 percent even after a late bid, with the big Nasdaq event still to come.

The narrow point about today played out roughly as I expected. I did not look for the first wave, the CRSP and Russell adds, to force a melt-up: that bid is small relative to current liquidity and fully telegraphed. And it did not. The stock sold off through the session and, despite a sharp late-day bid that tagged $190 in the final half hour, still closed down about 4 percent on the day. A scheduled, pre-positioned buy at the close is not the same as a surprise. Beyond that, the honest stance is two-sided. The option market is pricing daily moves of roughly 5 to 6 percent either way at a near 90 percent front-month vol, a one-month, one-sigma range of about $145 to $240, and its call skew says a real slice of the market is paying up for an inclusion day squeeze higher, not a fade. The reward and risk for new money here is plainly worse than it was at the IPO, but that is a long way from a confident short, and with the largest inclusion still ahead I am not calling the top.

The genuine directional catalyst is still on the calendar, and it is in August. After the first quarterly earnings the lockup cracks, and up to 20 to 30 percent of eligible insider shares, a pool several times the current float, become sellable for the first time, then in 7 percent steps through the autumn, with the bulk by December. SpaceX's $60 billion acquisition of the AI coding firm Cursor, announced around the listing, is expected to shift those lockup percentages slightly. The scarcity that makes this squeeze possible is itself on a published schedule, and the schedule starts to reverse in August. Only Musk stays locked, out to 2027.

The shape of it has not changed since I first wrote it down, it has only sharpened. A stock made artificially scarce by its lockup, bought on a published schedule by funds that cannot say no, already run some 40 percent by faster money before a forced dollar was spent, with an options market charging near 90 percent vol because no one can arbitrage it, and a skew that has rotated from fearing the lockup to chasing the inclusion. Today the first forced buyers showed up, and the big one follows in July. Much of the anticipated move is in, but with the biggest inclusion still ahead I would watch it run into the Nasdaq date rather than assume it is over, and keep the real reversal risk where it belongs, on the August lockup.

The dates are still on the board. Watch the calendar, not the rocket.

Disclosure. The author owns 100 shares of SpaceX, a small personal position unrelated to his academic work. He does not work for, consult for, or receive funding from SpaceX or any other company that would benefit from this article.

Not investment advice. Nothing in this piece is financial, investment, legal, or tax advice, and nothing here is a recommendation to buy, sell, or hold any security. The numbers and forecasts above are research outputs based on publicly available data and on the author's own calibrations; they carry meaningful uncertainty, can move with new information, and should not be relied upon for investment decisions. Past patterns do not guarantee future returns. Readers should consult their own qualified advisors before acting on any information in this article.

This article draws on the author's research on how index-driven demand moves stock prices: The Price of Passive Ownership and Indexing and the Elasticity of Stock Demand. Calculations are reproducible and available on request.

Comments or pushback? I read everything. Reply directly at behmaram.pouya@uqam.ca.

Subscribe

Like this? Get the next one by email.

One email per new article. No tracking, unsubscribe any time.

Comments? Reply at behmaram.pouya@uqam.ca.