How much SpaceX will the world be forced to buy, and what it will do to the price

The largest stock sale in history is a live experiment on a strange modern force: investors who must buy a stock, at almost any price, because it joins a list.

When SpaceX lists today at around $1.77 trillion, most of the coverage will be about Elon Musk. I want to ask something narrower and, I think, more revealing. Over the next few weeks, how much SpaceX will fund managers be forced to buy, simply to keep pace with the indexes their performance is judged against? Financial Times Alphaville put the number at about $14.2 billion. I make it closer to $9 billion, almost all of it from index funds rather than the stock pickers. Small as that sounds, it lands on so little tradable stock that it should still move the price hard, and I can put a figure on that move too, because the same method called Tesla's 2020 index jump almost exactly.

Here is the whole answer in one table. The rest of the piece explains where it comes from.

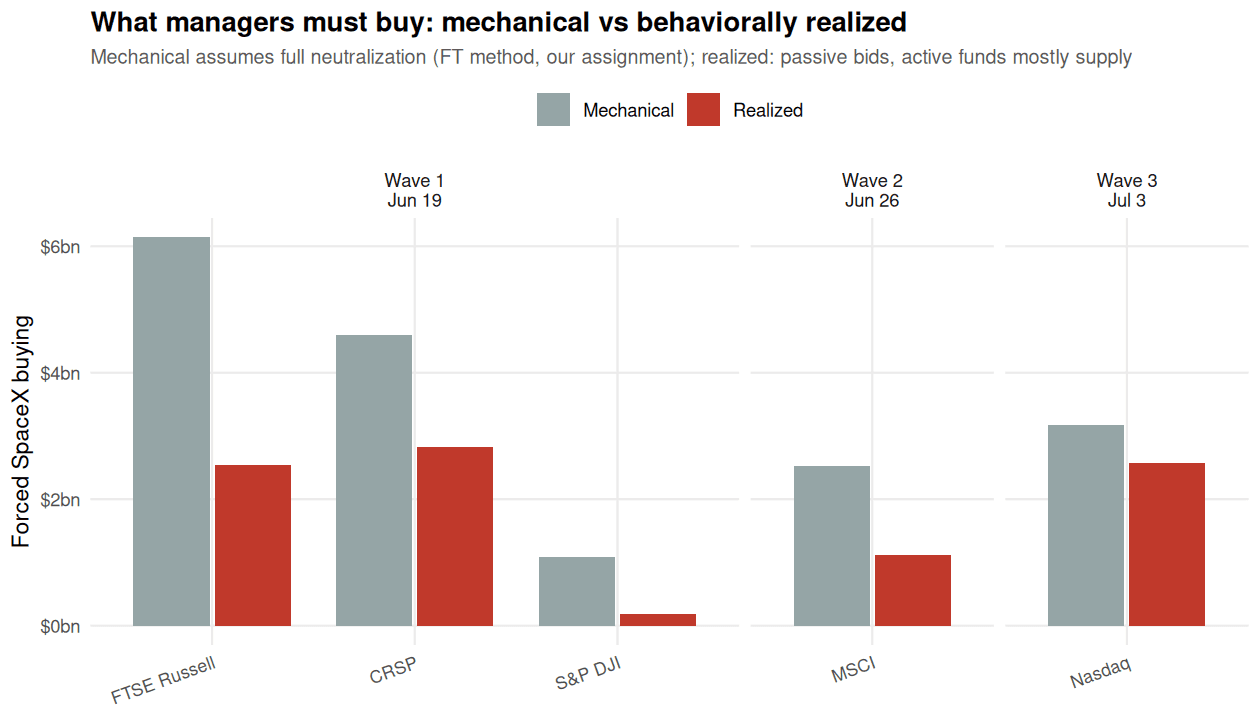

Forced SpaceX purchases by inclusion wave

Mechanical everyone neutralizes | Realized who actually buys | |

|---|---|---|

| Wave 1, June 19 · CRSP, Russell, S&P total market | $11.8bn | $5.6bn |

| Wave 2, June 26 · MSCI | $2.5bn | $1.1bn |

| Wave 3, July 3 · Nasdaq-100 | $3.2bn | $2.6bn |

| Total, funds worldwide | $17.5bn | $9.2bn |

| Of which US funds (the FT's scope) | $12.1bn | $5.9bn |

Forced SpaceX purchases by index inclusion wave. “Mechanical” assumes every benchmarked manager trades to index weight; “realized” applies buying rates estimated from 269 past index additions. Author's calculations.

Why anyone is forced at all

About a quarter of the US stock market sits in index funds, whose job is to mirror a list such as the Nasdaq-100. When a stock joins the list, those funds must own it, at whatever price the market sets. They do not ask whether it is cheap. They simply have to hold it, so joining a major index brings a guaranteed crowd of buyers.

The pressure does not stop at index funds, and that is where the big numbers come from. Any manager whose performance is judged against a benchmark is, in effect, short every stock they do not hold at its index weight. Sit out SpaceX, watch it climb, and you will be explaining to clients why you trailed the market. By that logic even stock pickers get pulled in, and that is how a few billion dollars of index fund buying turns into a headline figure of fourteen. Whether active managers really behave that way is something we can check rather than assume. Mostly, it turns out, they do not.

Three waves and a very thin float

Index providers rewrote their rulebooks for exactly this moment. SpaceX is set to enter the major index families on a fast track, in three waves: CRSP, Russell and the S&P total market indices about five trading days after listing, MSCI after ten, and the Nasdaq-100 after fifteen. The S&P 500 itself, with by far the most money tracking it, has kept its door shut for now. That single committee decision is worth about $11 billion of buying that is not happening yet.

The swing factor in every calculation is SpaceX's float. The company is worth $1.77 trillion, but only about $75 billion of stock will actually trade, under five percent, with the rest locked up for as long as a year. Nearly every major index weights its members by the value of shares that trade freely, not by the headline valuation:

That is why a $1.77 trillion company enters a $60 trillion index at a weight of barely a tenth of a percent. The exception is the Nasdaq-100, whose newly amended rule counts a company with very little float as if it were three times its tradable size. It reads like a safety valve and works like an amplifier.

Counting it from real portfolios

Sum across indices and the mechanical arithmetic is simple: each index's SpaceX weight times the money managed against that index,

The assets side is usually built from what funds say they track in their prospectuses. I built it instead from what roughly 32,000 funds worldwide actually hold, matching each one to the benchmark its portfolio really mirrors, using the holdings machinery from my research on passive ownership. Run the same assumption that everyone neutralizes through it and the US total comes to $12.1 billion, within about 15 percent of the $14.2 billion Alphaville reached from the opposite direction. Two independent routes landing that close is a good sign the mechanical number is sound.

The trouble is that it answers a hypothetical: what managers would buy if every last one of them traded to index weight. What I want is what they actually do, and for that the past is a reliable guide.

Who actually buys: the part a prospectus cannot tell you

I took 269 past additions to the Nasdaq-100 and the S&P 500, found every fund benchmarked to those indices, and measured how much of each newly added stock each fund actually bought in the months around inclusion, scaled by the stock's index weight. Write the realized demand as

where and are the fractions of the mechanical amount that passive and active funds truly trade. The pattern is stark. Passive funds deliver nearly the full amount, with around 0.93, measured the same way in both index families. Active funds barely move, with between 0.05 and 0.18 once you weight funds by size. Only about one active fund in twenty even holds a newly added name after it joins.

Apply those measured rates and the $17.5 billion mechanical ceiling falls to about $9.2 billion of realized buying worldwide, $8.4 billion of it from index funds and under $1 billion from active managers. The active half of the headline is the part that never arrives.

It is also worth going wider than the US. A count of American funds alone leaves out every foreign fund, and simply scaling up to global assets throws out a wild $51 billion that nobody should take seriously. My holdings are global to start with, so there is no scaling to do. Non-US funds benchmarked to these same indices, mostly the big cross-border vehicles run out of Ireland and Luxembourg, add roughly a quarter on top of the US figure. The forced bid reaches well beyond America, but it is nothing like a tidal wave.

From dollars to price: the Tesla calibration

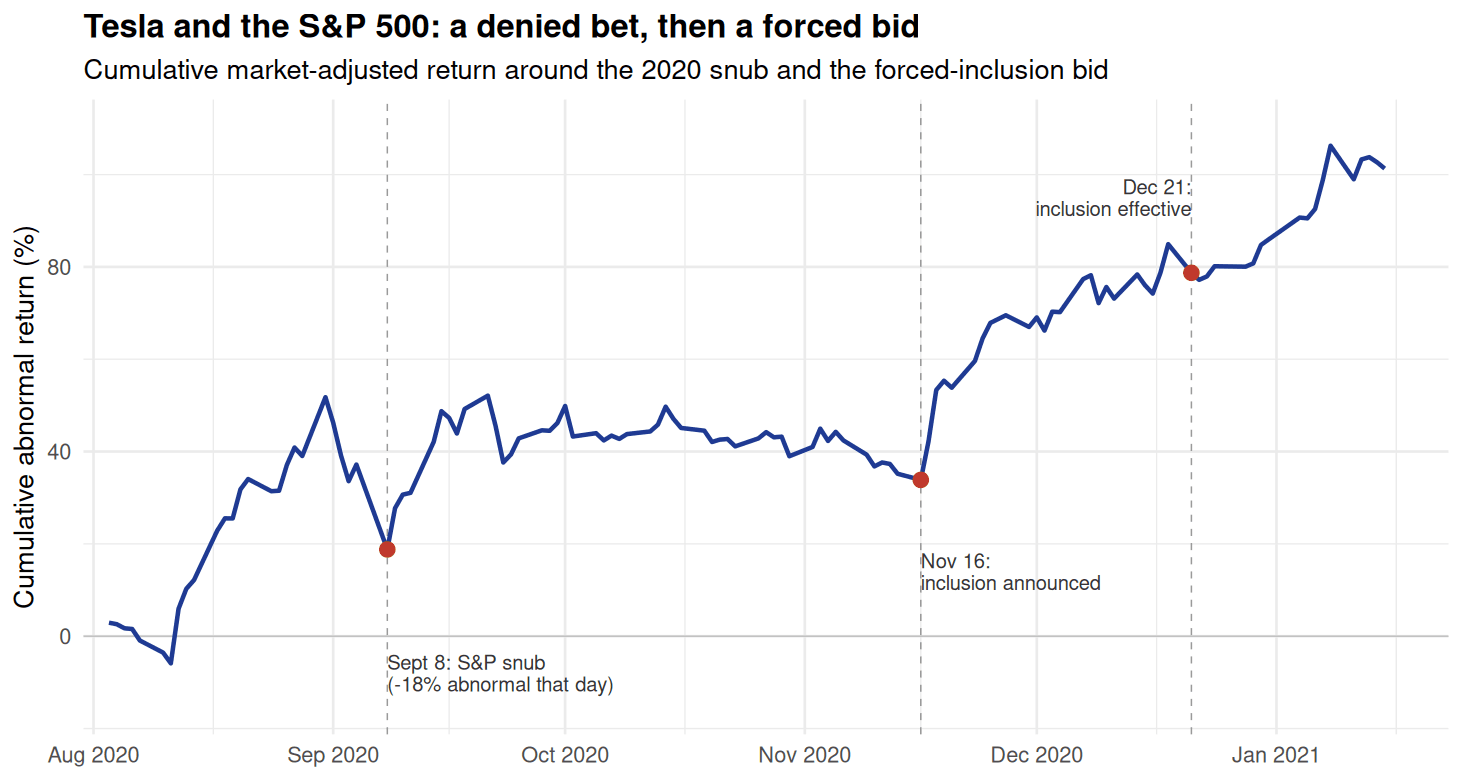

Counting the dollars is only half the job. What everyone actually wants to know is what that buying does to the price, and here Tesla hands us about as clean a test as markets ever offer. In September 2020 Tesla was eligible for the S&P 500, nearly everyone assumed it was a lock, and the committee said no. The stock fell about a fifth in a single day, which tells you how much of its price had been riding on forced buying that suddenly might not come. Two months later the committee relented. Index funds had to buy roughly $37 billion of Tesla, about a tenth of the company, and the framework I use turned that into a forecast through one relationship:

where the multiplier measures how stubbornly a stock's price resists new demand, estimated from a demand system fit to institutional holdings in my work on indexing and the elasticity of stock demand. For Tesla, my model predicted a 43 percent rise ahead of the event. The stock actually rose 40 percent between announcement and inclusion, so the forecast missed by about three percentage points. Across roughly 240 S&P 500 additions, the same pattern holds: bigger forced demand produces bigger inclusion jumps, in proportion.

SpaceX is the extreme version of the experiment

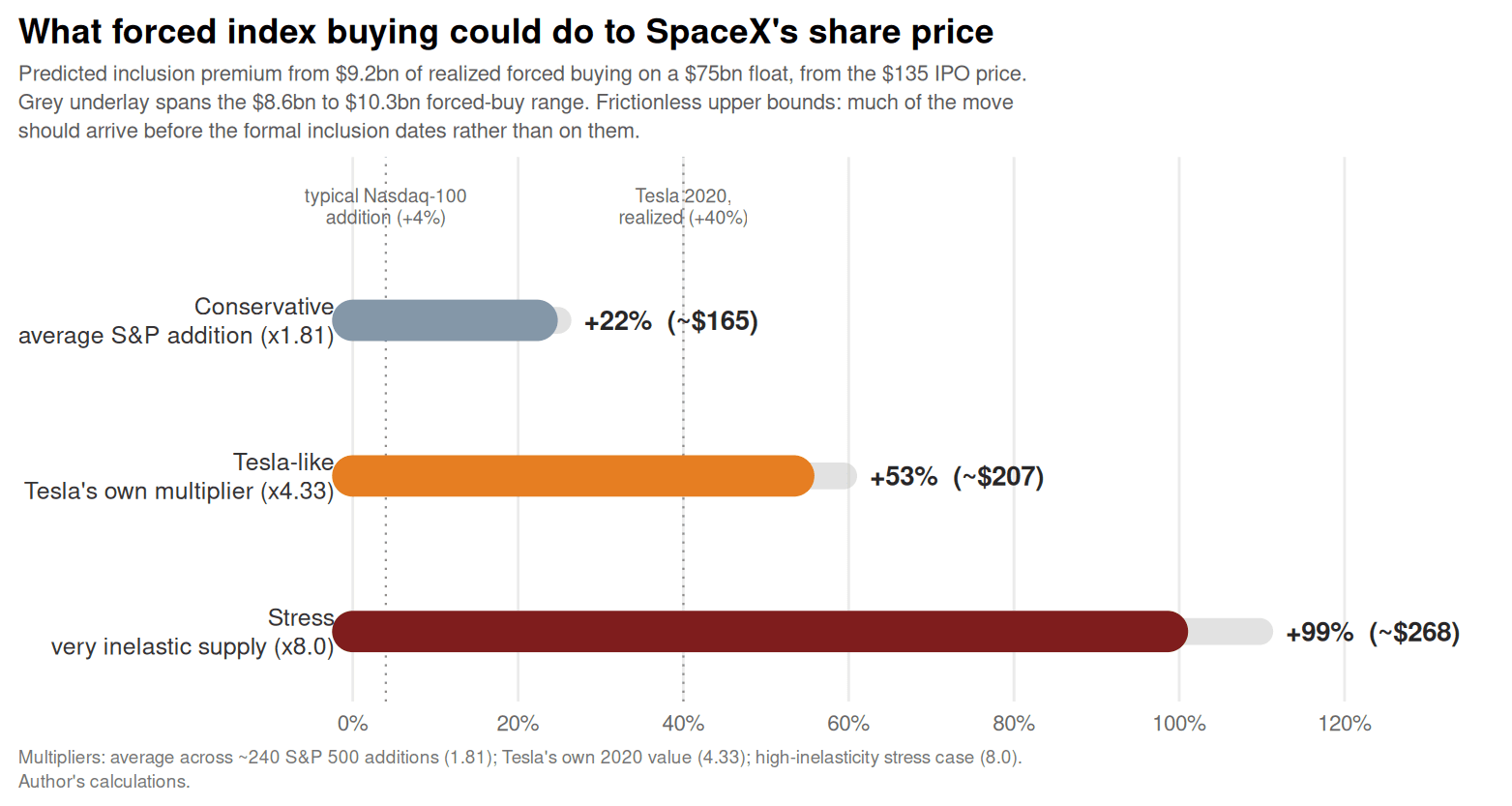

SpaceX pushes the same mechanism to its limit because of the denominator. Tesla's forced buying drew on a float of nearly its full market value. SpaceX's realized forced buying, about $9.2 billion, must squeeze through a $75 billion float: roughly an eighth of every tradable share, spoken for within three weeks of listing, by buyers who cannot say no.

Run that through the machinery I calibrated on Tesla and the frictionless inclusion premium is about 22 percent on a cautious multiplier and around 50 percent on a Tesla-like one. I would not bank the upper numbers, for three reasons that all push the same way. The rules and dates are public, so much of the move gets priced into the IPO and the run before inclusion rather than landing on the day itself. The IPO allocation itself hands shares to many of the funds that would otherwise buy in the market. And the sellers described above, active managers and short term speculators, return part of the float into the event. The honest forecast is a real inclusion premium in the double digits, most of it arriving early, not a clean pop on a single day.

How long does the jump last?

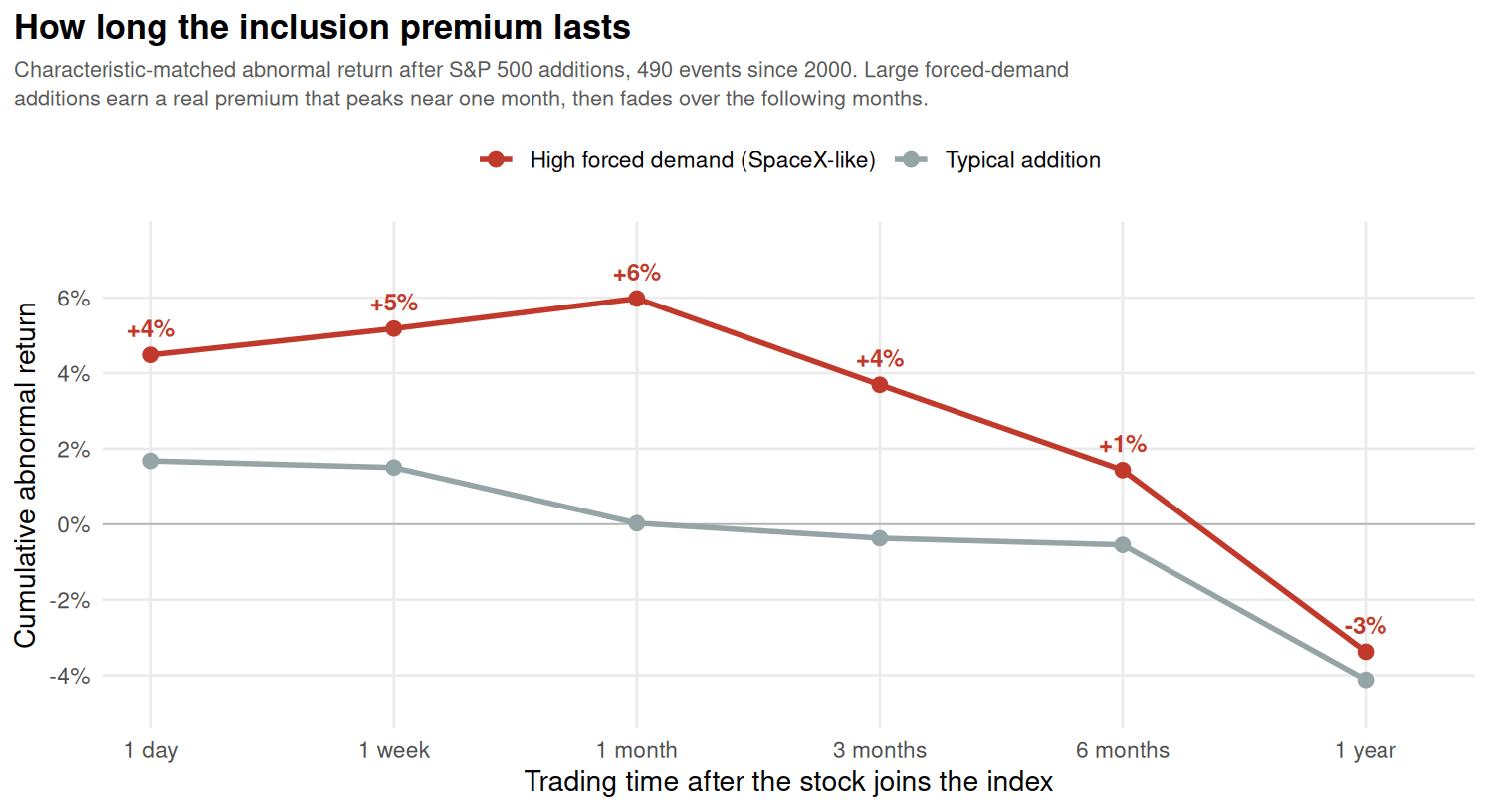

A premium that the buying creates is not the same as a premium that sticks. To see how long it survives, I tracked the abnormal return after 490 S&P 500 additions, comparing each added stock to similar stocks that were not added. The typical addition barely moves at all. The additions that came with large forced demand, the closest analog to SpaceX, are different: their premium builds to about 6 percent roughly a month after inclusion, then drains away over the next several months and is gone within a year. The forced bid lifts the price, and then ordinary supply and demand slowly take it back.

For SpaceX, I would expect that arc, steeper at both ends. The premium should be heavily front loaded, much of it showing up in the IPO itself and the days into inclusion rather than on the inclusion dates, exactly as Tesla rallied before its entry and slipped on the day. From there two forces pull against each other. As SpaceX's locked up shares unlock over the following months, the float grows and the scarcity that drove the premium eases, which argues for a fade. But the same growing float lifts SpaceX's weight in the Nasdaq-100, because the triple-float cap relaxes as more stock trades, so index funds must keep buying even as supply arrives. The net path is not a clean slide in one direction. My honest prediction is a sharp early premium, a partial giveback within the first few months as the history suggests, and a smaller residual that depends on how fast the lockups roll off against how fast the index weight climbs. The piece of the pop that rests purely on today's tiny float is the piece least likely to last.

So can you trade it?

If a wave of forced buying is coming, why not buy the float and ride it? Because everyone can see it coming. The rules are public, the dates are public, the thin float is obvious, and a move this well advertised tends to be priced before it arrives. Tesla is the cautionary tale. It soared in the weeks before inclusion, then fell about six percent on the very day the index funds finally bought. The money was made by investors who were early and sold into the forced bid, not by those who arrived for the main event. And even the early buyer, as the previous section showed, is buying a premium that history says mostly melts away within a year. The forced buying is real. It is not free money for whoever buys the offering.

The quiet power of the list makers

The lasting point is about who is in charge. Index providers used to be referees who kept the lists. A handful of rule changes now decide who must buy billions of dollars of a stock, on which day, and how hard that demand presses on a thin slice of shares. SpaceX is the first big test of that power, and the bigger one is already scheduled: the S&P 500 has kept its door closed, and SpaceX will walk through it the way Tesla did, once it shows a profit. When that happens, the forced bid will be several times larger than everything described here.

Method, data, and what could move these numbers

Every figure above is reproducible, and the machinery comes from two research papers. The fund holdings, benchmark assignment and index-ownership measurement are developed in The Price of Passive Ownership; the demand system behind the price multiplier is developed in Indexing and the Elasticity of Stock Demand. The forced buy is each index's SpaceX weight times the assets I measure tracking that index, summed across the published fast-track calendar; weights apply each provider's own float rule, with the Nasdaq tripling counted once. The realized haircut uses buying rates estimated from 269 historical additions across two index families, not assumptions. The price translation uses a demand multiplier validated on Tesla's 2020 inclusion and on roughly 240 S&P 500 addition events.

Four things could move the numbers, and I would rather flag them than have you find them. First, the final offer size, price and float shift every weight; I will refresh the estimates when the deal prices. Second, the index totals in the denominators are recent but not same-day, which matters at the ten percent level, not the order of magnitude. Third, funds benchmarked to global indices such as MSCI ACWI are not yet in my benchmark map, so the worldwide figure is, if anything, slightly conservative. Fourth, the price multiplier is borrowed, not measured, which is why the premium is a band. None of this changes the shape of the answer: a forced bid near $9 billion, delivered almost entirely by index funds, landing on a float thin enough to move the price by double digits, with most of that move arriving before the bell on inclusion day.

Disclosure. The author owns 100 shares of SpaceX, a small personal position unrelated to his academic work. He does not work for, consult for, or receive funding from SpaceX or any other company that would benefit from this article.

Not investment advice. Nothing in this piece is financial, investment, legal, or tax advice, and nothing here is a recommendation to buy, sell, or hold any security. The numbers and forecasts above are research outputs based on publicly available data and on the author's own calibrations; they carry meaningful uncertainty, can move with new information, and should not be relied upon for investment decisions. Past patterns do not guarantee future returns. Readers should consult their own qualified advisors before acting on any information in this article.

This article draws on the author's research on how index-driven demand moves stock prices: The Price of Passive Ownership and Indexing and the Elasticity of Stock Demand. Calculations are reproducible and available on request.

Comments or pushback? I read everything. Reply directly at behmaram.pouya@uqam.ca.

Subscribe

Like this? Get the next one by email.

One email per new article. No tracking, unsubscribe any time.

Comments? Reply at behmaram.pouya@uqam.ca.